Data-driven customer-centric Utilities of the (near) future

InterConnect can assist Utilities in developing, testing, and scaling up to their complete customer base innovative products that increase customers’ engagement through personalised data-driven flexible Demand Side Management services.

HERON

March 10, 2022A mantra in the energy retail business is that a Utility’s only purpose is to generate bills. However, modern Utilities must be multi-dimensional, with the capacity to excel in several aspects of their business domain to be successful. InterConnect can assist Utilities in developing, testing, and scaling up to their complete customer base innovative products that increase customers’ engagement through personalised data-driven flexible Demand Side Management services.

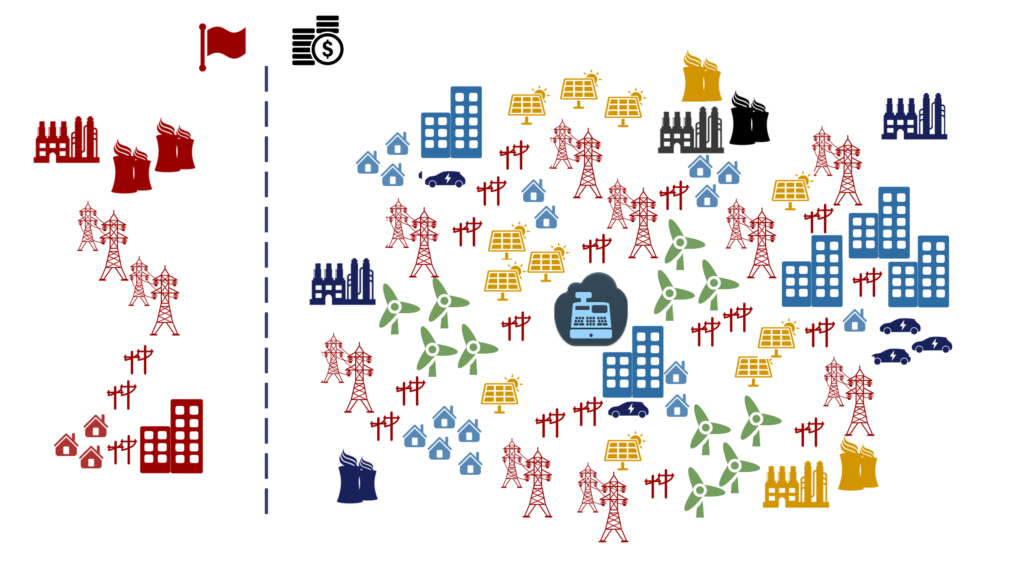

Almost three decades after the liberalisation of energy markets, the sector has evolved from state-owned monopolies operating across all aspects of the power system (generation, transmission, distribution, consumption) to a fragmented landscape consisting of multiple stakeholders, from high-tech specialised technology providers to financial institutions sensing new market opportunities with contradicting and often conflicting priorities and objectives.

Irrespective of how far countries have progressed into the transformation of their energy sectors, there have been extreme events such as market failures (California 2001), severe blackouts (UK 2019, Texas 2021), the production glut during Covid-19 lockdowns (2020-21) to name a few, that have questioned how consumers interact with electricity and their expectations of Utilities and System Operators. This has been more profoundly apparent in Europe during the latest months where the ongoing high electricity market prices crisis has allowed old wounds regarding the role of coal plants, the impact of renewables and the sanity of the market mechanisms to surface. Ιn this setting, Utilities are challenged as they attempt to diversify from well-established business models and practices to an environment involving new players assisted by more flexible regulatory frameworks, technological advances, and a shift in the public’s perception of electricity as a commodity in a period of crisis.

The electricity market transition from state-owned monopolies to a fully liberalised and decentralised market-based ecosystem.

The challenges Utilities are facing are further highlighted by the weakening of the fundamental assumption of the economics of Utilities regarding the low elasticity of the electricity price. Under the assumption of low elasticity, dominating Economic Theory since the 19th century, price changes do not lead to changes in demand given that a consumer is expected to consume electricity irrespective of its price. Time of Use tariffs have been gradually changing such perceptions with some consumers willing to shift towards night consumption, but ultimately the vast deployment of smart meters, dynamic tariffs, and Demand Response, all very recent developments, are creating a real shift in consumers’ behaviour, further pushing Utilities to evolve if they want to catch up with the developments.

This can be particularly difficult for them, which if cornered in the position of the incumbent, tend to favour risk-averse strategies given that they are structurally less agile due to their heritage and huge capital costs. This hesitancy has created new space for non-energy entities to compete, leading to existential threats for the established energy retailers as shown by the new players’ success in adapting, or even setting in some cases, the trends in digitalisation and decentralisation.

Big-Tech companies such as Google, Amazon, and Facebook, but also a massive collection of tech-savvy start-ups, are spearheading the effort in decarbonisation, energy efficiency and data-driven innovation. Moreover, the empowerment of the consumer, the abundant flow of information reinforced by social media and new digital channels of communication have brought immense competition. Such competition further reduces energy retailers’ already diminished profit margins, requiring costly retention and acquisition strategies to balance their customer base.

To navigate out of this position, Utilities have to accept that their traditional value chains (procure fuel, generate electricity, sell electricity) are forever disrupted and thus abandon their introvert tendencies that come from being the sole controllers of a commodity that is as necessary to our society as the air, water and nutrition is to our bodies. Instead of relics of the past, Utilities can become beacons of the future through investment in R&D activities that will allow them to dive into the ecosystem-driven world of technology and specialization. Such collaborations will develop innovative business models that will ultimately bring the much-required edge in their competition.

Utilities can turn the table by focusing on their strengths, which given that they are retailers, after all, is and always have been, their customers. Utilities do not have to become tech companies rivalling Google and the likes. Instead, they can remain – and if they haven’t been so far they should re-evaluate their strategy- customer-centric and focus on the digitalisation of their processes by letting data flow through every inch of their operations. For example, by harnessing troves of data linked to their customers, Utilities can provide personalised products and target specific segments of the wider population while building up green and sustainable credentials. Competitive electricity and natural gas offerings will have to be the core block of any innovative product but complemented by tailored services. Such services would focus on customers willing to install photovoltaics on their roof, those driving electric vehicles or for the early adopters who are very keen to embrace smart home, IoT and energy monitoring technologies and will allow the Utilities’ customer base to grow by improving customer experience and creating new markets. To achieve these targets, Utilities will have to invest not only in their digital infrastructure but also in collaborations that will turn them into orchestrators of technology-driven ecosystems. Assuming this role will ease the structural burden of having to develop digital platforms from scratch, allowing them to focus on their strengths and incrementally build digital infrastructure utilising their network of partnerships with specialised technology providers.

In this context, in HERON we acknowledge that we have much to gain through our involvement in InterConnect. As a member of the Greek pilot cluster, we collaborate closely with highly competent project partners contributing to a pool of knowledge and expertise, while expanding our network as a part of the wider consortium. From a technical perspective, operating as a Demand Response Aggregator we accumulate experience into operational and business challenges that are yet to appear in Greece. Being able to develop consumption monitoring tools and actively tap on the flexibility potential of Demand Response while integrating it on our existing systems, gives us the unique advantage of not only being ahead of the learning curve but also plotting it; a position that relatively few Utilities can claim.

Authors:

Athanasios Papakonstantinou, PhD is a Project Manager for European Projects within HERON’s Applied R&D function, a part of the Energy Management Division.

Sonae established a road map, based on the Science Based Targets initiative, that defines several pathways and measures to achieve carbon neutrality, many of them well aligned with InterConnect.